Mark Lazar’s June 2020 Newsletter

It is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own self-interest. Adam Smith

I’m fairly certain even Nostradamus could not have predicted the first half of 2020; a pandemic, followed by a near-total economic shutdown, the destruction of $12 trillion in stock valuation, a severe recession, unprecedented fiscal and monetary stimulus, and massive civil unrest, all followed by the fastest economic recovery in history. And we still have five months until the election. I can hardly wait to see what the second half of the year brings (insert smiley emoji here). Interesting times to be sure.

*All data as of 6/17/2020

After plunging nearly 35% domestically, and 49% internationally, markets are recovering at the fastest pace in history. And while the economy will likely take another two years to get back to where it was at the beginning of the year, markets are signaling a recovery is already underway. This may seem counterintuitive considering Q2 (April 1–June 30) GDP is expected to suffer the fastest drop in U.S. history. Ironically, we’ll experience both the worst economic compression and the fastest stock market recovery in the very same quarter. But as you already know, markets are forward-looking, and see beyond the current dour headlines and economic data.

Let’s take a moment to discuss several market indicators to gain a better sense of how markets can and do communicate expectations of the future:

The stock market is oftentimes a good canary in the coal mine. While stock prices tend to be more a function of (expected) earnings, corporate earnings and economic activity tend to be positively correlated, so a rising stock market today oftentimes is indicative of better economic days ahead.

S&P 500 3-Year History

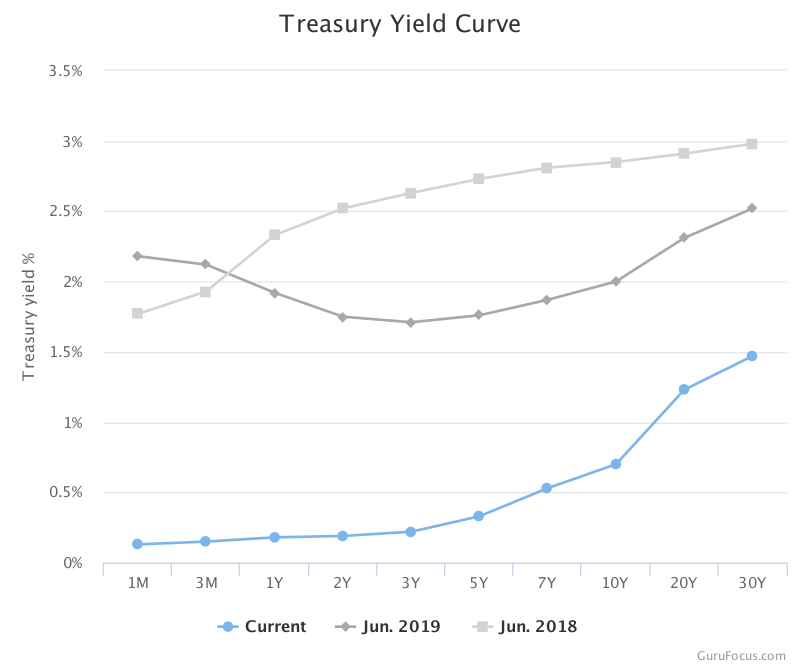

The Treasury yield curve is simply an X/Y graph of the interest rates/yields of government securities. With maturities ranging between 3-months and 30-years, the yield curve tells us not only the market’s expectations of future interest rates, but also of inflation, and economic growth; both of which are positively correlated with interest rates. While rates are currently near historical lows, the curve is upward-sloping, which is generally indicative of future positive economic growth and associated inflation. Conversely, a negative slope is oftentimes a harbinger of a recessions, while a flat curve implies little or no expected economic growth or inflation.

GuruFocus

Credit spreads, or the difference between a Treasury security (i.e. risk-free asset) and a corporate bond with the same maturity, communicate the required risk-premium, or additional return required for assuming credit risk (the risk of default by the issuer). When credit spreads widen it’s a risk-off trade; meaning the market is forecasting rising corporate defaults in the future. Conversely, when they’re narrowing, the opposite is true. You’ll notice in the chart below, spreads increased over 2% in a matter of weeks, followed by a drop of 1.4% in the past three months.

Federal Reserve Bank of St. Louis

While markets don’t always get it right, they tend to be good, unbiased prognosticators. But unlike pundits, politicians, and news agencies, markets don’t have an agenda or a dog in the fight; their only concern is profit. Like Cuba Gooding Jr.’s character in the 1990s comedy, Jerry Maguire, the market’s mantra is the same; “Show me the money.” While some may denounce a profit motive, believing it lacks virtue, by the same token, a profit motive benefits from purity of purpose and objectivity. I don’t want markets to be virtuous; I want them to be efficient. Instead, I believe it’s the responsibility of investors to be virtuous with their profits.

Mark Lazar, MBA

Certified Financial Planner®

www.pathwaytoprosperity.com

Show Me the Money

Mark Lazar’s June 2020 Newsletter

It is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own self-interest. Adam Smith

I’m fairly certain even Nostradamus could not have predicted the first half of 2020; a pandemic, followed by a near-total economic shutdown, the destruction of $12 trillion in stock valuation, a severe recession, unprecedented fiscal and monetary stimulus, and massive civil unrest, all followed by the fastest economic recovery in history. And we still have five months until the election. I can hardly wait to see what the second half of the year brings (insert smiley emoji here). Interesting times to be sure.

*All data as of 6/17/2020

After plunging nearly 35% domestically, and 49% internationally, markets are recovering at the fastest pace in history. And while the economy will likely take another two years to get back to where it was at the beginning of the year, markets are signaling a recovery is already underway. This may seem counterintuitive considering Q2 (April 1–June 30) GDP is expected to suffer the fastest drop in U.S. history. Ironically, we’ll experience both the worst economic compression and the fastest stock market recovery in the very same quarter. But as you already know, markets are forward-looking, and see beyond the current dour headlines and economic data.

Let’s take a moment to discuss several market indicators to gain a better sense of how markets can and do communicate expectations of the future:

The stock market is oftentimes a good canary in the coal mine. While stock prices tend to be more a function of (expected) earnings, corporate earnings and economic activity tend to be positively correlated, so a rising stock market today oftentimes is indicative of better economic days ahead.

S&P 500 3-Year History

The Treasury yield curve is simply an X/Y graph of the interest rates/yields of government securities. With maturities ranging between 3-months and 30-years, the yield curve tells us not only the market’s expectations of future interest rates, but also of inflation, and economic growth; both of which are positively correlated with interest rates. While rates are currently near historical lows, the curve is upward-sloping, which is generally indicative of future positive economic growth and associated inflation. Conversely, a negative slope is oftentimes a harbinger of a recessions, while a flat curve implies little or no expected economic growth or inflation.

GuruFocus

Credit spreads, or the difference between a Treasury security (i.e. risk-free asset) and a corporate bond with the same maturity, communicate the required risk-premium, or additional return required for assuming credit risk (the risk of default by the issuer). When credit spreads widen it’s a risk-off trade; meaning the market is forecasting rising corporate defaults in the future. Conversely, when they’re narrowing, the opposite is true. You’ll notice in the chart below, spreads increased over 2% in a matter of weeks, followed by a drop of 1.4% in the past three months.

Federal Reserve Bank of St. Louis

While markets don’t always get it right, they tend to be good, unbiased prognosticators. But unlike pundits, politicians, and news agencies, markets don’t have an agenda or a dog in the fight; their only concern is profit. Like Cuba Gooding Jr.’s character in the 1990s comedy, Jerry Maguire, the market’s mantra is the same; “Show me the money.” While some may denounce a profit motive, believing it lacks virtue, by the same token, a profit motive benefits from purity of purpose and objectivity. I don’t want markets to be virtuous; I want them to be efficient. Instead, I believe it’s the responsibility of investors to be virtuous with their profits.

Mark Lazar, MBA

Certified Financial Planner®

www.pathwaytoprosperity.com