May 2023

“Allow a government to decline paying its debts and you overthrow all public morality and unhinge all principles that preserve the limits of free constitutions.” Alexander Hamilton

*Market index data as of 4/30/2023

The debt ceiling is once again in the spotlight. Last month the House passed the Limit, Save, Grow Act which would raise the current $31.4T debt cap, but impose spending cuts over the coming decade. Upon hearing the news, Senator Chuck Schumer told reporters the House bill is “dead on arrival” and the measure “only brings us dangerously closer” to a default. House leader Kevin McCarthy responded, “We can have reckless spending, or we can have responsibility, but we can’t have both. We can leave our children a future with higher inflation, higher interest rates, and crushing debt, or we can leave them free to pursue happiness as God intended.”

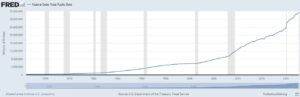

Federal Reserve Economic Data

With rare exception, debt limit fights follow the same, old banal script; the minority party champions fiscal responsibility whereas the Administration bemoans catastrophic consequences if they are unable to spend every dollar on their wish list. With rare exception, neither are playing it straight.

Just to clarify, the deficit represents the difference between federal revenues and outlays, and increases the national debt by the same amount. According to the Congressional Budget Office the national debt will increase $20.6T between now and 2033. This figure was revised ~20% higher just since last May. Now for the really bad news; the CBO historically underestimates future deficits by a large margin. Why? Because their models fail to include recessions, geopolitical events, pandemics, and the like.

| Year |

2023 |

2024 |

2025 |

2026 |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

2033 |

Total |

| Deficit |

$1.4T |

$1.4T |

$1.4T |

$1.4T |

$1.4T |

$1.9T |

$1.8T |

$2.1T |

$2.3T |

$2.5T |

$2.9T |

$20.6T |

CBO 10-Year Budget Forecast

Since 1965 federal spending (as a percent of GDP) has increased 55%, which is remarkable since much of the nation’s major infrastructure projects (highways, bridges, rail lines, dams, etc.) had already been built by then. The single biggest reason for the increase; federal entitlements.

Uncle Sam’s spending can be broken down as follows; 62% is deemed mandatory, 28% discretionary, and 10% net interest. The elephant in the room is clearly “mandatory” spending, with entitlement programs (SS, Medicare, and welfare) comprising 52% of the federal budget. Social Security is metaphorically referred to as the third rail of politics, but it now appears all federal programs are sacrosanct and off the table in terms of budget discussions. Just to be clear, the term budget cut in Washington-speak represents a cut in the rate of spending growth, not a reduction in nominal dollars.

Budgeting isn’t rocket science. Every successful company, agency, non-profit and household does it. However, Washington bureaucrats have proven themselves to be unwilling, inept, or both, and have failed in their most basic duty—fiscal responsibility—for decades. Clearly political self-interest supersedes leadership and neither party is willing to take away the punch bowl for fear of losing the next election.

While it’s easy to get distracted by the current worrisome headlines, the real concerns looming on the horizon are:

- The Social Security Trust Fund runs out of money by 2034 and, if not fixed, benefits will be reduced by 20%. This shouldn’t come as a surprise to anyone. In 2009 Boston College published a short article entitled, The Social Security Fix-It Book, which (then) projected the SS Trust Fund would be depleted by 2037, and provides a variety of simple suggestions as to how to restore solvency.

- The Medicare trust fund will be depleted by 2028; five years from now. Here’s a link to a very good article that’s easier to understand than the official Medicare trustee’s report.

- Depending on the report, unfunded pension liabilities range between $1.3T and $8.3T. For example, CalPERS’ (the nation’s largest public pension with more than 2 million members) funded ratio dropped to 74%, meaning the plan will have less than three-quarters of the assets needed to pay for pensions already promised to workers.

When Earnest Hemingway was asked how he went bankrupt, he famously quipped, “Two ways; gradually and then suddenly.” In the physical world, engineers use a methodology known as fracture mechanics to identify and predict the failure of a component or structure due to an existing crack or flaw. Bridges, buildings dams and the like can be structurally sound for decades if not centuries but, analogous to Hemingway’s financial downfall, when subjected to an undue stress can collapse quite suddenly. Economic systems are no different. Economies that on the surface appear robust will lose integrity and eventually become unstable absent fiscal responsibility, sound monetary policy, rule of law, and property rights. The prosperity that many take for granted requires a culture that promotes and rewards merit, hard work, innovation, capital, and risk-taking. As nations move further away from these ideas and principles, the greater the risk of catastrophic failure.

High inflation, a pending recession, bank failures, and a tumultuous stock market, aren’t problems; rather, they’re symptoms of unsound, unsustainable policies. Over the coming decade we will be facing BIG issues that if ignored will unquestionably become actual crises. They’re fixable today, but real solutions (as opposed to stopgap measures) require both sides be open to discussion, operate in good faith, and have a genuine willingness to compromise.

Mark Lazar, MBA

Certified Financial Planner™

Pathway to Prosperity

Fracture Mechanics

May 2023

“Allow a government to decline paying its debts and you overthrow all public morality and unhinge all principles that preserve the limits of free constitutions.” Alexander Hamilton

Item

Dow Jones Ind Avg

8.59%

EAFE Foreign Index

2.16%

Barclays Agg Bond Index

2.19%

3.4%

*Market index data as of 4/30/2023

The debt ceiling is once again in the spotlight. Last month the House passed the Limit, Save, Grow Act which would raise the current $31.4T debt cap, but impose spending cuts over the coming decade. Upon hearing the news, Senator Chuck Schumer told reporters the House bill is “dead on arrival” and the measure “only brings us dangerously closer” to a default. House leader Kevin McCarthy responded, “We can have reckless spending, or we can have responsibility, but we can’t have both. We can leave our children a future with higher inflation, higher interest rates, and crushing debt, or we can leave them free to pursue happiness as God intended.”

Federal Reserve Economic Data

With rare exception, debt limit fights follow the same, old banal script; the minority party champions fiscal responsibility whereas the Administration bemoans catastrophic consequences if they are unable to spend every dollar on their wish list. With rare exception, neither are playing it straight.

Just to clarify, the deficit represents the difference between federal revenues and outlays, and increases the national debt by the same amount. According to the Congressional Budget Office the national debt will increase $20.6T between now and 2033. This figure was revised ~20% higher just since last May. Now for the really bad news; the CBO historically underestimates future deficits by a large margin. Why? Because their models fail to include recessions, geopolitical events, pandemics, and the like.

CBO 10-Year Budget Forecast

Since 1965 federal spending (as a percent of GDP) has increased 55%, which is remarkable since much of the nation’s major infrastructure projects (highways, bridges, rail lines, dams, etc.) had already been built by then. The single biggest reason for the increase; federal entitlements.

Uncle Sam’s spending can be broken down as follows; 62% is deemed mandatory, 28% discretionary, and 10% net interest. The elephant in the room is clearly “mandatory” spending, with entitlement programs (SS, Medicare, and welfare) comprising 52% of the federal budget. Social Security is metaphorically referred to as the third rail of politics, but it now appears all federal programs are sacrosanct and off the table in terms of budget discussions. Just to be clear, the term budget cut in Washington-speak represents a cut in the rate of spending growth, not a reduction in nominal dollars.

Budgeting isn’t rocket science. Every successful company, agency, non-profit and household does it. However, Washington bureaucrats have proven themselves to be unwilling, inept, or both, and have failed in their most basic duty—fiscal responsibility—for decades. Clearly political self-interest supersedes leadership and neither party is willing to take away the punch bowl for fear of losing the next election.

While it’s easy to get distracted by the current worrisome headlines, the real concerns looming on the horizon are:

When Earnest Hemingway was asked how he went bankrupt, he famously quipped, “Two ways; gradually and then suddenly.” In the physical world, engineers use a methodology known as fracture mechanics to identify and predict the failure of a component or structure due to an existing crack or flaw. Bridges, buildings dams and the like can be structurally sound for decades if not centuries but, analogous to Hemingway’s financial downfall, when subjected to an undue stress can collapse quite suddenly. Economic systems are no different. Economies that on the surface appear robust will lose integrity and eventually become unstable absent fiscal responsibility, sound monetary policy, rule of law, and property rights. The prosperity that many take for granted requires a culture that promotes and rewards merit, hard work, innovation, capital, and risk-taking. As nations move further away from these ideas and principles, the greater the risk of catastrophic failure.

High inflation, a pending recession, bank failures, and a tumultuous stock market, aren’t problems; rather, they’re symptoms of unsound, unsustainable policies. Over the coming decade we will be facing BIG issues that if ignored will unquestionably become actual crises. They’re fixable today, but real solutions (as opposed to stopgap measures) require both sides be open to discussion, operate in good faith, and have a genuine willingness to compromise.

Mark Lazar, MBA

Certified Financial Planner™

Pathway to Prosperity